Wall Street closes at a record for the first time since end of January

Introduction & Market Context

Shiseido Co., Ltd. (TYO:4911) released its full-year 2025 results and 2026 outlook on February 10, 2026, revealing a mixed financial performance that triggered a 2.64% drop in its share price to ¥2,782.5. While the Japanese beauty giant exceeded its profit targets, sales momentum remained challenged in certain regions, particularly the Americas.

The company’s presentation highlighted significant progress in its structural reforms and cost management initiatives, which helped drive profitability improvements despite top-line pressure. These results come amid ongoing geopolitical tensions between Japan and China that continue to impact the travel retail segment.

Executive Summary

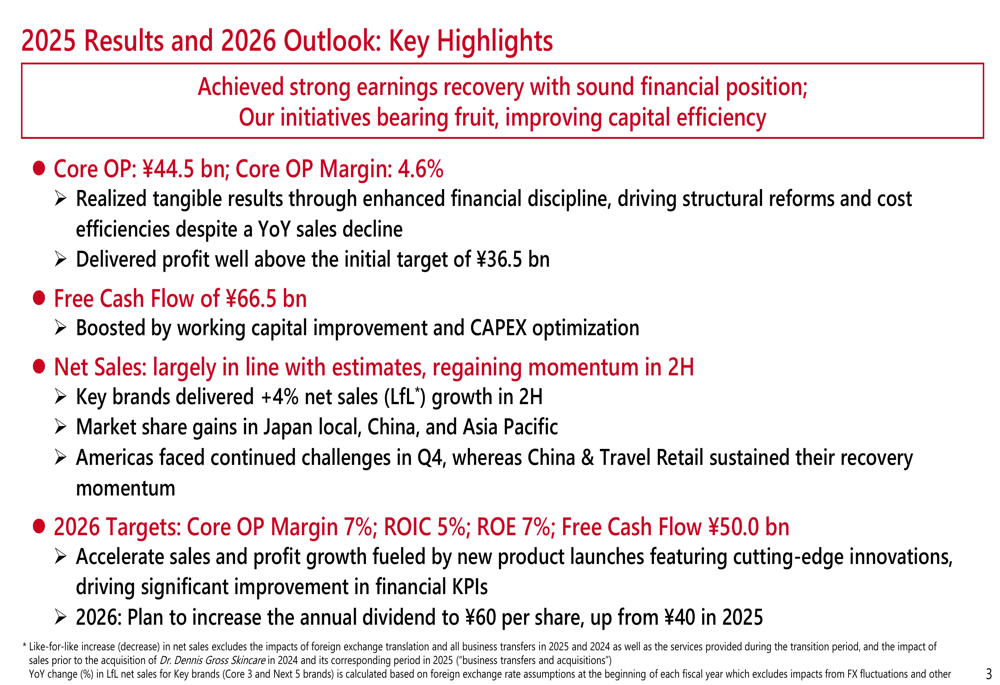

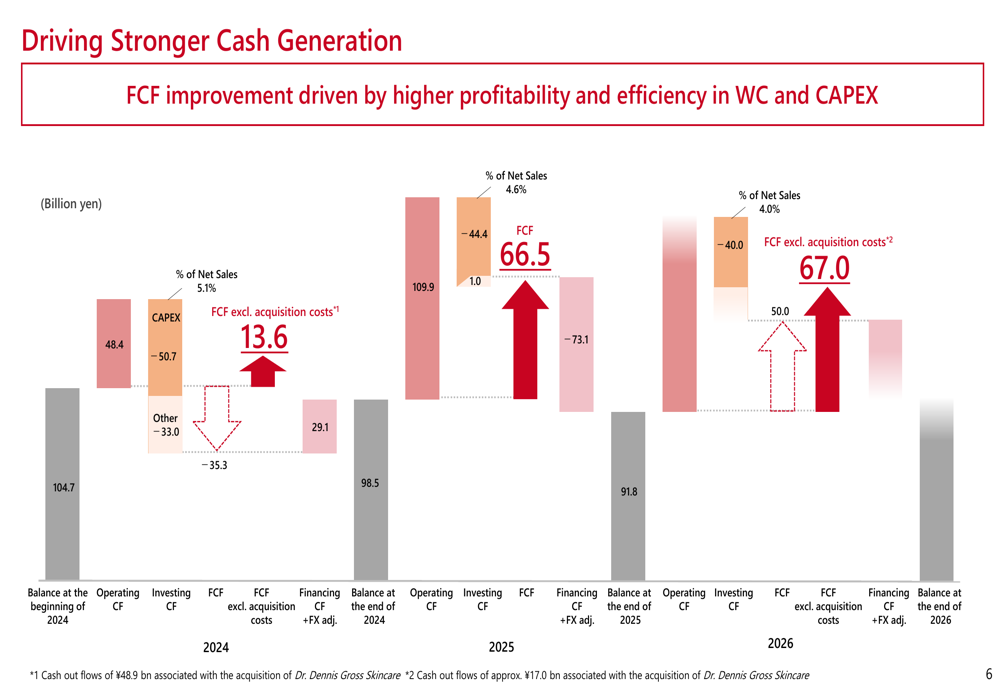

Shiseido reported core operating profit of ¥44.5 billion for FY2025, representing a margin of 4.6% and exceeding the company’s initial target of ¥36.5 billion. Free cash flow saw substantial improvement, reaching ¥66.5 billion, boosted by working capital enhancements and capital expenditure optimization.

As shown in the following comprehensive overview of 2025 results and 2026 outlook:

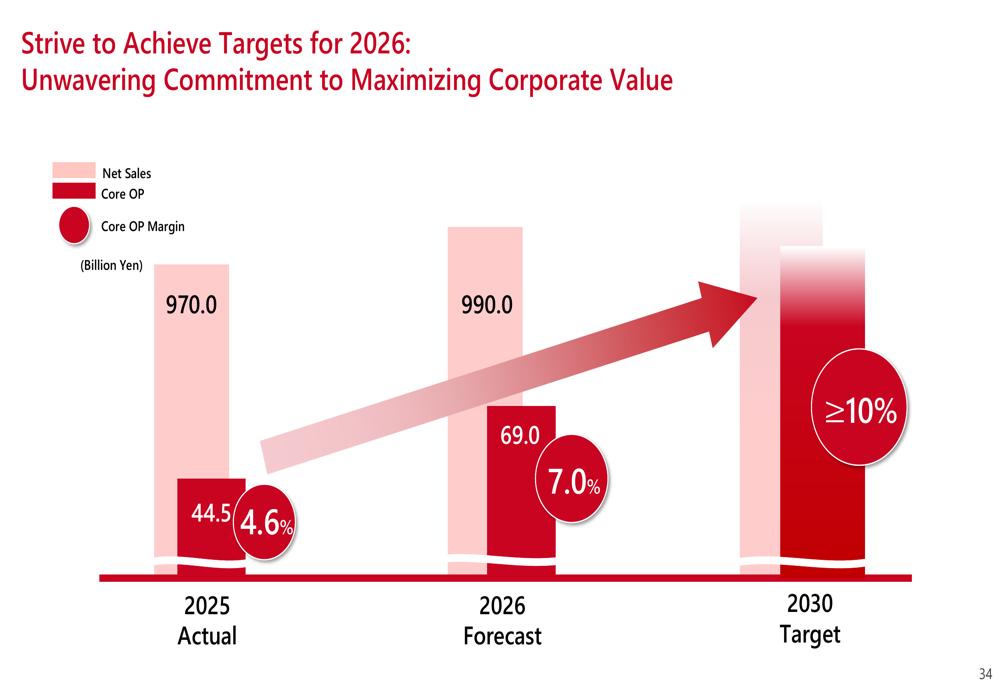

Net sales for the year were ¥970 billion, largely in line with company estimates but representing a real growth rate decline of 2% year-over-year. However, Shiseido noted that key brands delivered 4% net sales growth in the second half of 2025, with market share gains in Japan, China, and Asia Pacific regions.

Detailed Financial Analysis

The company’s 2025 financial performance reflects its ongoing transition toward a more profitable business model. While sales declined, Shiseido’s focus on high-margin products and cost efficiency drove significant profit improvements.

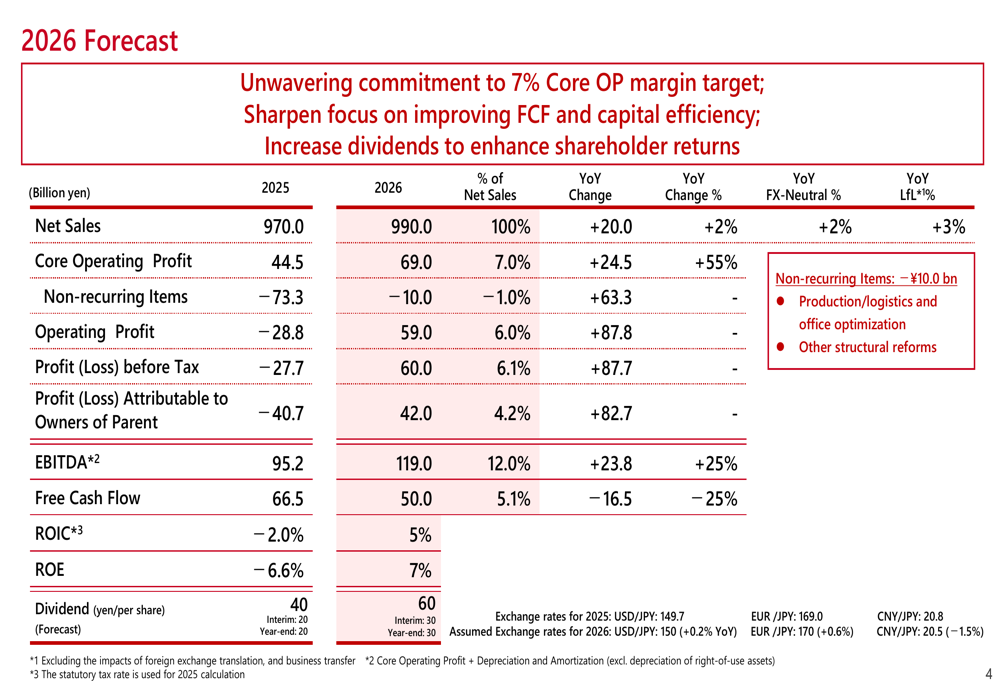

The detailed 2026 forecast reveals ambitious targets for continued profit expansion:

For 2026, Shiseido is projecting net sales of ¥990 billion, representing 2% year-over-year growth (3% on a like-for-like basis). More impressively, core operating profit is expected to surge 55% to ¥69 billion, with the margin expanding to 7.0%. The company also anticipates EBITDA of ¥119 billion (+25% YoY) and free cash flow of ¥50 billion.

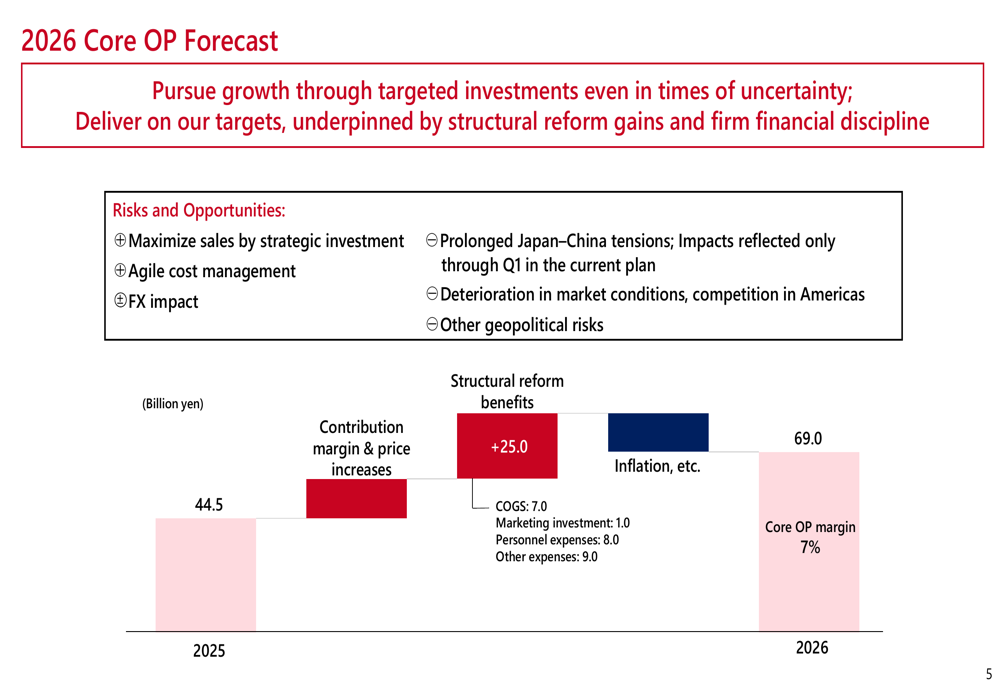

The following breakdown illustrates how Shiseido expects to achieve its 2026 core operating profit target:

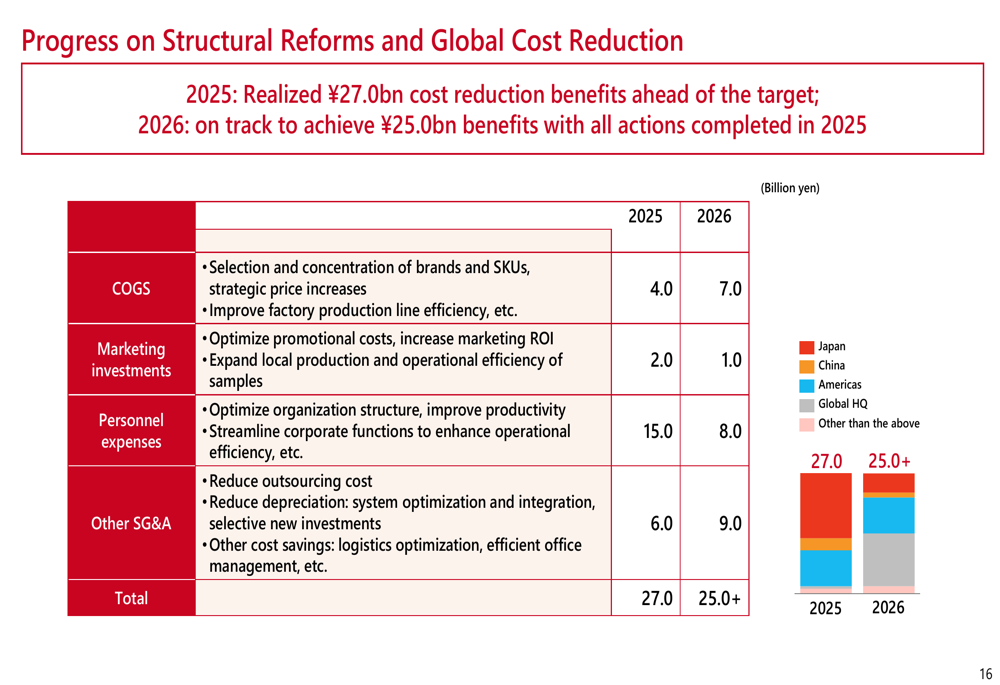

Structural reform benefits are projected to contribute ¥25 billion to the 2026 core operating profit, highlighting the significant impact of the company’s cost-cutting initiatives. However, the presentation also acknowledges potential risks, including prolonged Japan-China tensions, deteriorating market conditions, and other geopolitical factors.

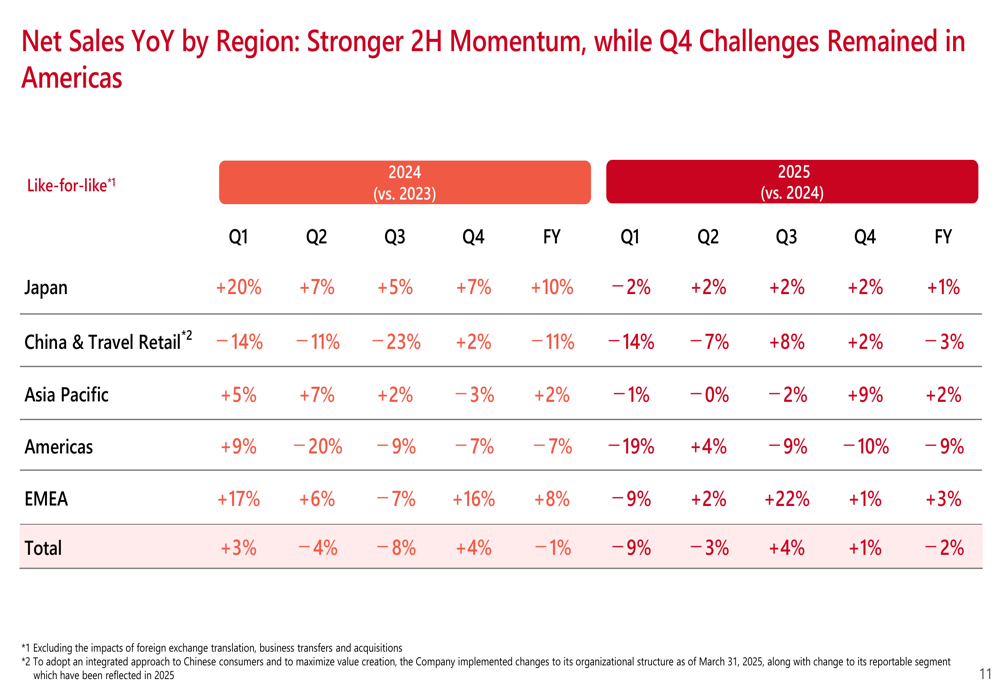

Regional performance varied significantly across markets. Japan, China, and Asia Pacific showed stronger results, while the Americas faced continued challenges. The company’s net sales by region reveals this divergence:

Strategic Initiatives

Shiseido’s presentation emphasized several strategic initiatives driving its transformation toward higher profitability and capital efficiency. The company is focusing on generating stronger cash flow through improved profitability and capital management:

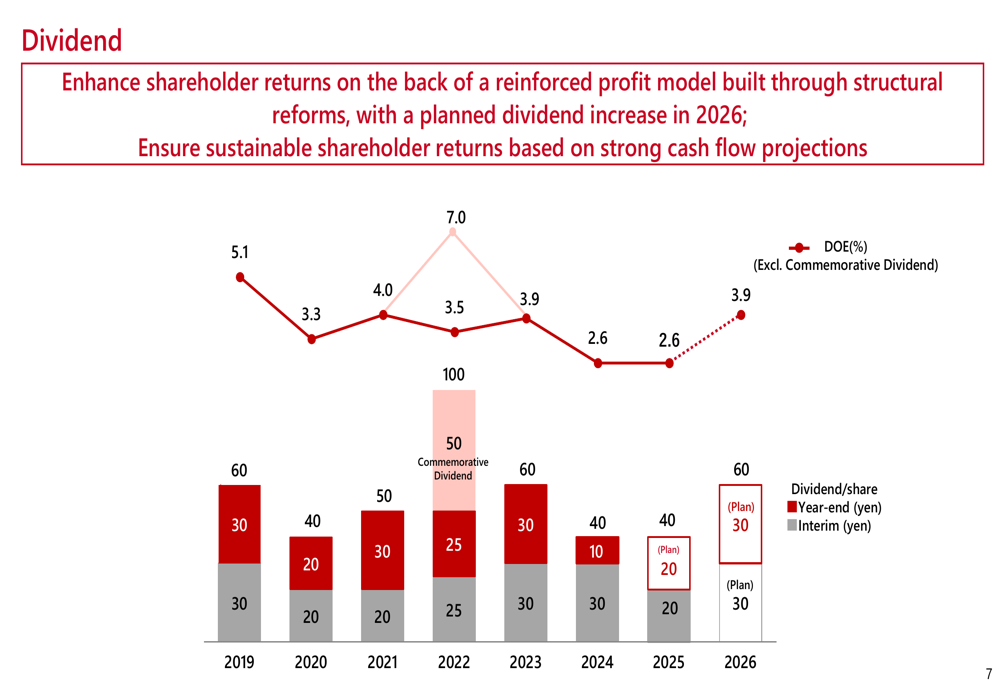

Shareholder returns are also a priority, with plans to increase the annual dividend from ¥40 per share in 2025 to ¥60 per share in 2026:

The company’s structural reforms and global cost reduction efforts are yielding tangible results across multiple expense categories:

These initiatives are part of Shiseido’s broader strategy to transform into a leaner, more efficient organization. The company reported that net sales per employee have increased by approximately 30% from 2021 to 2025, reflecting significant productivity improvements.

Forward-Looking Statements

Looking ahead, Shiseido has set ambitious targets for 2026 and beyond, with a long-term goal of achieving a core operating profit margin of 10% or more by 2030:

During the earnings call, CEO Kentaro Fujiwara emphasized that "2026 is not a year of reform, but a year to reliably deliver growth." The company plans to leverage its technology-driven innovation and balanced global structure to drive sustainable growth.

Shiseido’s strategy involves concentrating investments in high-profit brands, particularly its core brands (SHISEIDO, Clé de Peau Beauté, NARS) and next brands (ELIXIR, ANESSA). The company also outlined a turnaround plan for Drunk Elephant to address performance challenges.

Despite the optimistic outlook, investors should note several risks that could impact Shiseido’s ability to achieve its targets. These include continued softness in the Japanese market, geopolitical tensions affecting travel retail, and potential market uncertainties. The stock’s negative reaction to the earnings announcement suggests investors may be concerned about the company’s ability to deliver on its sales growth projections amid these challenges.

Nevertheless, Shiseido’s demonstrated progress in improving profitability and cash flow generation, combined with its clear strategic focus on high-margin brands and operational efficiency, positions the company to potentially overcome these headwinds and deliver on its long-term profit targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.